Welcome to

On Feet Nation

Members

-

Michael Kyle Online

-

-

Blog Posts

Top Content

Not known Facts About How Do Mortgages Work With Married Couples Varying Credit Score

Editorial Note: Forbes might make a commission on sales made from partner links on this page, however that doesn't affect our editors' viewpoints or examinations. Simply weeks prior to the new year, mortgage rates are exceeding yet again. Home loan rates on the 30-year fixed-rate mortgage fell to their least expensive point for the 14th time this year, slipping to 2.

The new record might be a bit of a surprise, as the bond market livened up on Tuesday following whisperings of financial relief. Treasury yields, which typically relocate tandem with home loan rates, rose slightly, however did not bring house loan rates with them. With home loans in high demand and the refinance share of mortgage applications up 102% year-over-year, lender revenues are skyrocketing, according to a current report by the Home loan Bankers Association.

This, coupled with an aggressive fiscal policy from the Federal Reserve, is what's keeping a cover on rates. "The Federal Reserve's expected plans to continue their pace of mortgage-backed securities purchases is also most likely to keep upward movements in home mortgage rates in check," states Matthew Speakman, an economist at Zillow.

Home mortgages to purchase a home were up 9% https://codyvtun222.skyrock.com/3344960948-All-about-How-To-House-Mortgages-Work.html week-over-week, after adjusting for the Thanksgiving vacation, and were 28% higher than the very same time in 2015, according to the Mortgage Bankers Association's (MBA) Weekly Mortgage Applications Survey for the week ending Nov. 27, 2020. The extreme real estate lack has actually pressed the average purchase loan quantity to $375,000, the greatest level given that MBA started its study in 1990.

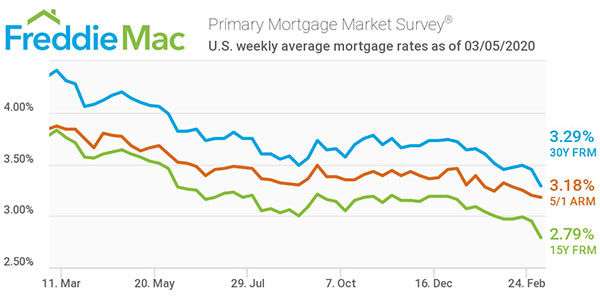

"The continual duration of low home loan rates continues to spark borrower demand, and the home mortgage industry is poised for its greatest year in originations since 2003," says Joel Kan, associate vice president of financial and industry forecasting for MBA. "The continuous re-finance wave has been beneficial to homeowners aiming to reduce their month-to-month payments throughout these challenging economic times came up with by the pandemic." The typical rate for the criteria 30-year fixed dropped one basis point to 2.

The Main Principles Of Why Are Most Personal Loans Much Smaller Than Mortgages And Home Equity Loans?

A basis point is one one-hundredth of a percentage point. This time last year, the 30-year repaired was 3. 68%. Borrowers with a 30-year fixed-rate mortgage of $300,000 with today's interest rate of 2. 71% will pay $1,218. 38 per month in principal and interest (taxes and costs not included), the Forbes Advisor mortgage calculator programs.

60. That very same mortgage gotten a year ago would cost an additional $57,269. 11 in interest over the life of the loan. The average interest rate on the 15-year fixed mortgage dropped two basis points last week to 2. 26%. This time last year, the 15-year fixed-rate mortgage was at 3.

Customers with a 15-year fixed-rate home loan of $300,000 with today's rate of interest of 2. 26% will pay $1,966. 65 each month in principal and interest (taxes and fees not included). The overall interest paid over the life of the loan will be $53,997. 26. The typical rate on a 5/1 variable-rate mortgage fell 30 basis indicate 2.

16% recently. what are interest rates today on mortgages. In 2015, the 5/1 ARM was 3. 39%. ARMs are home mortgage that have an interest rate that varies with the marketplace. In the case of 5/1 ARMs, the first 5 years have a set rate and then switch to a variable rate after that. That means when the average rate increases or falls, so will your rate.

Home mortgage rates are at record lows, so this might be an opportune time for lots of folks who desire to conserve cash on their home mortgage or re-finance their current mortgage. If you're re-financing, understand you might pay a somewhat greater interest rate since of a brand-new refinancing charge. Borrowers who wish to get the least expensive rate need to make certain they have a credit rating of a minimum of 760.

Not known Factual Statements About What Is The Current Apr For Mortgages

In truth, debtors with lower credit rating can be charged one portion point or more greater than borrowers with really great or excellent scores. Before you get a mortgage, check your credit rating. Lots of banks and credit cards permit you to do this free of charge. One method you can enhance your score fairly quickly is to pay for financial obligation.

In addition to your credit rating, loan providers will look at your debt-to-income ratio, or DTI. This is your overall monthly debt divided by your gross monthly earnings. It's generally a picture of just how much you owe versus just how much you earn. The lower your DTI, the much better possibilities you have of getting a lower rates of interest.

Finally, research studies have actually shown that individuals who go shopping around tend to get lower rates than those who get a home mortgage from the very first lending institution they talk with. Know what the existing typical rate of interest is along with what your credit rating, earnings, financial obligation and expenditures are prior to you begin applying.

As the Federal Reserve concludes a two-day conference Wednesday, it will be fighting with how to react to opposing forces in the country's COVID-19-fueled financial crisis. On the one hand, a renewal of the virus already has slowed the economy and an even darker winter lays ahead. At the very same time, wide accessibility of a vaccine by spring provides the prospect of a considerable improvement.

However Fed authorities still have more ammunition, largely related to their enormous bond-buying stimulus intended at holding down long-term rates that impact home mortgages and other loans. The Fed's policy choice, which will be launched at 2 p. m. on Wednesday, is anticipated to center around those bond purchases-- and it could imply slightly lower regular monthly costs for homebuyers and other debtors.

The Of What Banks Use Experian For Mortgages

Here's the breakdown of what the Fed may do: The Fed is now acquiring $80 billion in Treasury bonds and $40 billion in mortgage-backed securities monthly, putting downward pressure on long-lasting rate of interest, such as for mortgages and business bonds. The average maturity of the securities it's purchasing is 7.

/find-and-compare-best-mortgage-rates-4148342_FINAL-d90ea8095a49474f90bee793bf4c5918.png)

Some financial experts expect Fed officials to buy the very same amount of bonds but shift the mix towards those with longer maturities. That would inject more stimulus into the economy by more pushing down rates for mortgages, business bonds and other types of loans. COVID-19 is increasing across the nation, with cases, hospitalizations and deaths reaching new records.

Job development slowed greatly in November and initial jobless claims, a rough procedure of layoffs, leapt sharply to 947,000 the week ending December 5."The economy really needs," more stimulus, states Oxford economic expert Kathy Bostjancic. "Fed officials may see the winter season infection revival as the apparent moment to shoot their last bullet," Goldman Sachs said in a research study note. This creates a tidal wave of brand-new work for home loan loan providers. Sadly, some loan providers do not have the capability or workforce to process a large number of refinance loan applications. In this case, a lender might raise its rates to deter new company and provide loan officers time to process loans currently in the pipeline.

Cash-out refinances pose a greater risk for home mortgage lenders, so they're typically priced greater than brand-new house purchases and rate-term refinances. Because rates can vary, always search when buying a house or re-financing a relinquish timeshare ownership home loan. Comparison shopping can potentially save thousands, even tens of thousands of dollars over the life of your loan.

Some just opt for the bank they use for examining and cost savings because that can seem simplest. However, your bank may not offer the best mortgage offer for you. And if you're re-financing, your monetary situation might have altered enough that your present loan provider is no longer your best choice.

Which Bank Is The Best For Mortgages Fundamentals Explained

When searching for a home loan or re-finance, lenders will provide a Loan Estimate that breaks down essential costs associated with the loan. You'll wish to read these Loan Price quotes thoroughly and compare Find out more expenses and fees line-by-line, consisting of: Rate of interest Yearly portion rate (APR) Monthly mortgage payment Loan origination costs Rate lock costs Closing costs Keep in mind, the least expensive interest rate isn't always the finest deal.

It estimates your overall annual cost including interest and charges. Likewise pay attention to your closing costs. Some lending institutions might bring their rates down by charging more in advance via discount rate points. These can add thousands to your out-of-pocket expenses. You can also negotiate your home loan rate to get a much better offer (how does chapter 13 work with mortgages).

Lender An uses the better rate, however you prefer your loan terms from Loan provider B. Talk to Lender B and see if they can beat the former's pricing. You may be amazed to discover that a loan provider is willing to offer you a lower rate of interest in order to keep your organization.

Mortgage debtors can pick between a fixed-rate home loan and an variable-rate mortgage (ARM). Fixed-rate home mortgages (FRMs) have rate of interest that never ever alter, unless you choose to refinance. This leads to predictable month-to-month payments and stability over the life of your loan. Adjustable-rate

Views: 3

Comment

© 2024 Created by PH the vintage.

Powered by

![]()

You need to be a member of On Feet Nation to add comments!

Join On Feet Nation